A good CIBIL score is crucial for securing loans and credit cards with favorable terms. One of the key components of your credit report is the Days Past Due in CIBIL report, which reflects your loan repayment behavior. Understanding the Days Past Due in CIBIL report for students is very important as it may impact the education loan approval negatively and the loan may get rejected if there are multiple late payments.

In this blog we will we will understand about DPD, Days Past Due in CIBIL report in detail along with its meaning in banking, full form, types, method of calculation and how it impacts our loan processing.

Table of Contents

- What is Days Past Due in CIBIL Reports?

- What is DPD Full Form in CIBIL Report?

- What are the Types of Days Past Due(DPD)?

- How DPD in CIBIL Report Affects Your Education Loan?

- How to Improve DPD in CIBIL Report?

- How to Calculate Days Past Due in Banking?

- How to Find Days Past Due in CIBIL Report?

- How to Report Discrepancy in DPD?

- Conclusion on Days Past Due(DPD)

- FAQ on DPD in CIBIL Report

What is Days Past Due in CIBIL Reports?

Days Past Due in CIBIL report indicates how many days a payment has been delayed after a missed EMI. DPD is a critical factor in determining your CIBIL score and can impact loan approvals, including education loans. If your CIBIL report shows one or more DPD entries, lenders may perceive you as a high-risk borrower. However, the impact depends on the type of DPD in CIBIL report, as different banks and financial institutions assess overdue payments differently. The longer a payment remains overdue, the more it negatively affects your DPD in CIBIL report and, in turn, your overall creditworthiness.

Before approving an education loan, banks review the CIBIL report or credit report to assess the borrower’s repayment behavior and credit utilization habits. Your creditworthiness is primarily evaluated based on your DPD status, making it crucial to monitor your Days Past Due in CIBIL Report regularly. To improve your chances of securing a loan, ensure timely repayments and maintain a healthy credit profile.

What is DPD Full Form in CIBIL Report?

The DPD full form in the CIBIL report is “Days Past Due.” It represents the number of days a borrower has delayed paying their loan EMI or credit card bill. In banking, DPD (Days Past Due) is a crucial factor in assessing a borrower’s repayment history and financial discipline.

Lenders use the Days Past Due in CIBIL Report to evaluate whether an individual has been consistent with loan repayments. It reflects the borrower’s payment behavior over the last 36 months (3 years). If your DPD in the CIBIL report consistently shows ‘000’, it means you have made timely payments with no missed EMIs.

Importance of DPD in Banking

DPD in banking report helps lenders or banks assess a borrower’s creditworthiness. A high Days Past Due value in a CIBIL report can negatively impact your credit score, making it difficult to obtain new loans or credit cards. DPD entries appear for various types of loans, including:

- Home Loans

- Personal Loans

- Credit Cards

- Education Loans

Frequent delays in EMI payments increase the Days Past Due in CIBIL Report, leading to a negative impact on your credit history. If your DPD is consistently high, lenders may consider you a risky borrower, potentially resulting in loan rejection or higher interest rates.

Regular credit monitoring helps keep your DPD in check. It is advisable to pay all the EMI on time so that any type of education loan defaulter legal actions can be avoided. You can improve your DPD by making timely payments on all outstanding dues.

DPD Example

To understand Days Past Due in CIBIL report, let’s look at a real-life example:

Akash took an education loan from ABC Bank. The repayment has started and the date of the EMI deduction is the 10th of every month. The account from which the EMI was supposed to be deducted was not funded and it bounced due to insufficient funds. Now, the bank sends reminder calls and messages to Akash to pay the EMI with penalties. Akash paid the EMI on the 18th of that month. This difference of 8 days is called DPD (full form: Days Past Due).

In case you have missed your EMIs once or twice, it will be negative but the lender may consider approving the loan. If you are facing any problem in repaying the loan then immediately contact the lender and apply for an education loan restructure because maintaining a low days past due (DPD full form in loan) is crucial for maintaining a healthy credit profile.

What are the Types of Days Past Due(DPD)?

Credit bureaus like CIBIL track your DPD closely. The credit report shows different types of DPD in CIBIL Report depending on the repayment made by the borrower. The DPD value is based on the delayed repayment of a certain period.

You can understand the types of Days Past Due(DPD) values shown in the credit report in the table given below:

| DPD Value | Impact on Credit Score | Meaning |

|---|---|---|

| XXX | Positive | Capable of repaying on time/all payments have been made on time/bank’s failure to update the payment |

| 000 | Positive | No outstanding payment is left for the loan or credit card |

| STD | Negative | Dues are less than 90 days |

| SUB | Worse | The account was NPA for less than 12 months |

| DBT | Worse | The account was NPA for 12 months |

| LSS | Worse | Loss Identified and the lender has lost hope of repayment |

What is STD and SUB Status in CIBIL Reports?

When reviewing a CIBIL report, different terms are used to classify credit accounts based on repayment behavior. Knowing these terms helps maintain a healthy credit profile.

What is STD in CIBIL?

The STD full form in cibil is stands for “Standard”, An STD in cibil means that payments have been made on time or within 90 days of the due date. This indicates good credit behavior and does not negatively impact your CIBIL score.

What is SUB in CIBIL?

The fullform of SUB is stands for “Sub-Standard”. Sub std in cibil is a classification indicates that payments are overdue by more than 90 days. This suggests a higher credit risk, which can negatively impact loan approvals and interest rates.

Other Important Credit Report Classifications:

- SMA (Special Mention Account): Accounts that are still standard but show early signs of financial stress, requiring closer monitoring.

- DBT (Doubtful): Accounts that have remained sub-standard for more than 12 months, indicating prolonged financial distress.

- LSS (Loss): Accounts where dues are considered uncollectible by the lender.

Why Maintaining an STD Status is Important?

Keeping your credit account under the STD (Standard) category ensures a good CIBIL score and improves your chances of securing loans at favorable terms. On the other hand, an SUB (Sub-Standard) status can indicate financial trouble, making it difficult to get credit approvals in the future.

How DPD in CIBIL Report Affects Your Education Loan?

When you apply for an education loan, the first thing the bank will do is to pull out your credit report and check it thoroughly. If the bank finds a negative Days Past Due(DPD) like STD(Standard) or SUB(Sub-standard) status, your loan may get rejected. Based on the credit history, the banks decide education loan amount.

Improving your CIBIL rating involves reducing your DPD. Even if your overall credit score is good but there are negative DPDs, your loan will be straightaway rejected. The banks and financial institutions take DPD in CIBIL Report very seriously while approving the loan. Once they sense high risk, they won’t approve the loan.

30 Days Past Due in Credit Report

A delay in loan repayment always impacts your credit score negatively. The bank or the financial institution from where you have taken the loan reports even the shortest delay to the credit information companies or the credit bureau. If there is 30 days past due in credit report, your loan might get rejected as it will be a risk indicator for the lender and they will consider that your repayment behaviour is not good. As a responsible borrower, you should always focus on how to increase the CIBIL score.

60 Days Past Due on Credit Report

60 days past due on credit report acts as a high risk indicator. This means that you have missed paying the EMI for 2 months or more and your loan account was treated as a SSA (sub standard asset). This may be the worst case for your credit history as you will find it very difficult to get fresh loans in future. It will also create hindrance if you apply for education loan refinance or restructure.

Also Read: Loan rejected despite having good credit score? Check this blog and understand why your education loan got rejected even if your credit score is good

How to Improve DPD in CIBIL Report?

A negative Days Past Due in credit score will close the doors for all future loans. It is very important to understand how to avoid any single negative DPD in the report. To avoid negative DPD in CIBIL report, follow the major guidelines to maintain a healthy credit score:

- Pay EMIs on Time – Set up auto-payments or reminders to ensure timely repayments.

- Keep Enough amount in Loan Account: Keep the bank account funded 4-5 days prior to the date of the EMI deduction.

- Avoid Late Payments on Credit Cards – Even a few missed payments can increase your Days Past Due and lower your creditworthiness.

- Reduce Outstanding Debt – Maintain a low credit utilization ratio to improve your overall credit health. Negotiate with Lenders – If facing financial difficulties, communicate with lenders for loan restructuring options.

- Avoid utilising the maximum limit of credit cards as it will increase the burden due to which you may delay the repayment.

- Choose a safe date for EMI deduction at the time of getting the loan. Make sure that your salary or any other payment gets credited before that date so that you won’t face a lack of funds.

How to Calculate Days Past Due in Banking?

Monitoring days past due(DPD) is very valuable and important for good credit health. DPD or Days Past Due is calculated by finding the difference between the date of the EMI deduction and the date on which the borrower paid the missed EMI. The amount overdue in the Cibil report is a negative sign for both the borrower and the lender. Check the details of the calculation below:

Formula to Calculate Days Past Due(DPD)

The formula to calculate DPD directly depends on the due date and selected payment date:

DPD = Actual Payment Date – Due Date

For example, the EMI is scheduled to be deducted every month on the 5th. For some reason, the borrower failed to keep the account funded and EMI bounced. The borrower paid the EMI on the 26th of that month. Here, the DPD will be 26 days – 5 days = 21 days.

Here, there is a difference between the EMI deduction date and the date on which payment was made is 21 days. Hence, the days past due(DPD) will be 21 days. DPD affects your credit utilization negatively.

Also Read: Always stay informed about the regulations set by RBI. Check this blog and know the latest RBI regulations on Credit Reports to Credit Information Companies.

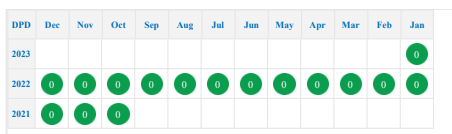

How to Find Days Past Due in CIBIL Report?

You can find the DPD in credit report by checking the ‘payment history’ section. DPD will be mentioned separately for each credit account.

To check DPD in credit report, follow the steps mentioned below:

- Download your CIBIL report from authorised portals like ET Money, WishFin etc, Paytm etc

- Check the credit or loan accounts

- Go through the ‘Payment History’ section

- For all the timely repayments, you will see ‘0’ marked in green colour

How to Report Discrepancy in DPD?

Sometimes you may notice a discrepancy in your credit report regarding the DPD value. This happens because sometimes there is a delay in updating the status of the report of a borrower. You may notice that you have made the payment on time but it does not show ‘000’ as the DPD.

Immediately report the error to the credit bureau explaining the entire case.

To know more details on discrepancy in DPD, refer the following:

- If it has been marked negative, it will appear in deep orange or red colour

- Check the same and match it with your EMI payment date

- If there is a discrepancy, immediately report to the bureau mentioning the name of the lender, loan account number and transaction ID

- The credit bureau will mark that account as ‘under dispute’

- A proper verification will be made involving the bank or the lender and the borrower

- If its a discrepancy, the bureau will update the same and it will start reflecting as ‘000’

- If your credit score has dropped due to discrepancies, the same will be updated along with the DPD value

Conclusion on Days Past Due(DPD)

The Days Past Due (DPD) metric is an important factor in credit score calculations. Practicing financial discipline ensures timely repayments and a strong credit profile. Check the following conclusion on the discussion over Days Past Due(DPD) given below:

- Days Past Due is the full form of DPD.

- Your credit report summary shows your DPD details and how much delay was there in your payments.

- Your financial behaviour is evaluated by looking at your DPD.

- High loan delinquency is straight up related to the increased DPD.

- Your creditworthiness is assessed with Days Past Due(DPD).

- Simply a high DPD will indicate that greater credit risk is there to lenders.

- For everyone, it is suggested to have a good repayment track record.

- It is a Debt repayment pattern.

- It is suggested to ensure that there are no errors in your DPD.

FAQ on DPD in CIBIL Report

Days Past Due CIBIL report is the total number of days that indicates the delay in loan repayment (if any). It shows the difference between the actual date of payment and the auto-debit EMI date which was missed by the borrower due to insufficient funds in the bank account.

DPD, or Days Past Due, refers to the number of days a borrower has delayed in making a loan or credit card payment. The Days Past Due in CIBIL Report is recorded monthly and plays a crucial role in determining an individual’s creditworthiness. A higher DPD negatively impacts the CIBIL score, making it harder to secure loans or credit approvals.

You cannot directly remove Days Past Due in a CIBIL Report, as it is a record of your repayment history for the past 36 months. However, if the DPD entry is due to an error, you can raise a dispute with CIBIL to correct it. If it is accurate, the best way to reduce its impact is by making timely payments, clearing outstanding dues, and maintaining a strong credit history. Over time, consistent repayments will improve your credit score and enhance your chances of loan approval.

STD refers to any overdue of less than 90 days which is a negative indicator. It is difficult to get any kind of loan approved if there is a negative DPD in CIBIL. The lenders consider it as a high risk and reject the loan application.

Timely repayments, low credit card use and a lesser number of enquiries are some of the major ways to improve your credit score. Maintaining a low DPD is the key as a high DPD will lead to a negative credit score.

If you notice any discrepancy in your Days Past Due in the CIBIL report, it is crucial to report it immediately to the credit bureau. Ensure that your dispute request includes details such as your loan account number, lender’s name, payment history, and a brief explanation of the error. Correcting an incorrect DPD in the CIBIL report can help maintain a healthy credit score and improve your chances of loan approval.

The Days Past Due in a CIBIL report is calculated by subtracting the payment date from the due date. The formula to determine DPD is:

DPD = Payment Date – Due Date

If the payment is made after the due date, the number of days delayed will reflect in the CIBIL report under the DPD section. A higher DPD can negatively impact your CIBIL score, affecting your creditworthiness and loan approvals.

Days Past Due(DPD) in CIBIL is important because it speaks about a borrower’s creditworthiness and financial discipline. Banks use the DPD to check requirements on whether to sanction a loan or not.

It can be difficult to get a loan from a private bank if your credit report shows a 60-day DPD in the repayment of any previous loans.

DPD (Days Past Due) and a delinquent mark on a credit report are related but not exactly the same thing.

– DPD refers to the number of days a payment on an account is overdue. It indicates how many days past the due date a payment is.

– A delinquent mark on a credit report usually occurs when an account is significantly past due, often around 30 or more days.

Derogatory marks and days past due in CIBIL (Credit Information Bureau India Limited) reports indicate different aspects of a borrower’s credit history. Derogatory marks refer to serious negative items such as loan defaults, bankruptcies, or accounts sent to collections, which damage credit scores and remain on the report for several years. On the other hand, days past due represent the number of days a payment is overdue beyond its due date.

STD in CIBIL means a credit account with payments made on time or within 90 days of the due date. It reflects responsible credit behavior, helping maintain a good credit score. The STD full form in CIBIL is Standard, and it assures lenders of timely repayments.

SUB-STD in CIBIL refers to a credit account where payments are overdue by more than 90 days. The SUB-STD full form in CIBIL is Sub-Standard, indicating a higher credit risk due to prolonged payment delays.

This was all about understanding the DPD or Days Past Due in the CIBIL report. Always make your EMI payments and credit card bills on time so that your credit score remains good.

| Related Blogs |

|---|

| Impact of Loan Restructure on Credit Score |

| Credit Scores and Their Impact on Education Loan Refinancing |

| Importance of Maintaining a Good Credit Score |

Follow Us on Social Media