Credit Scores and Their Impact on Education Loan Refinancing: Credit scores are used by banks or financial institutions to determine your repayment behaviour and the details of loan outstanding. A credit score of 6.5 and above is considered a good credit score which helps you get loans easily. When you plan for loan refinancing it is very important to have a good credit score. If you have started repayment for the existing loan and making all the payments on time without any delay your credit score will ultimately increase. This particular repayment history will be checked by the new bank/lender to analyse your repayment behaviour. Let’s understand in detail the impact of credit scores on education loan refinancing.

Table of contents

What is a Credit Score and How it Works?

Credit score determines your creditworthiness by showing your repayment behaviour and history. On the basis of these details, you get a score between 300 to 900, where 900 is considered an exceptional score. Usually, a credit score above 6.5 and above is a good score that you get after making timely repayments against your loans and credit cards. The scores are calculated based on four major categories:

- Credit History: This section shows all kinds of credit accounts which you have had in the past or ongoing. If you have a credit card, ongoing EMIs, or any past loans this section will show everything.

- Accounts History: This section will show the entire detail of all your loan accounts including the name of the lender, EMI amount, late payments (if any), number of EMIs, date on which the account was opened etc.

- Public Record: This category of credit history shows big financial errors made by you including bankruptcy. It will also show criminal details (if exist) in your record.

- Credit Enquiries: Credit enquired shows any kind of enquire made by a lender/bank/financial institution to check your creditworthiness.

Also Check: How to Claim Tax Exemption from Education Loan

Impact of Credit Score on Education Loan Refinancing

The credit score always has a direct impact on any kind of loan you are taking from a bank or any financial institution. No lenders will provide you with a loan or a credit score without analyzing your credit history. A high credit score will get you a loan approved quickly. With a low credit score, you won’t be getting loans easily. When you plan to get a takeover education loan you must have a high credit score.

The new bank will check the previous payment record that you made as EMI against the existing education loan. After checking the credit history the bank will approve the loan refinance if the credit score is good i.e. above 6.5 or 7 subject to the terms and conditions of the bank. Let’s check some of the benefits of a good credit score and its impact on education loan refinancing:

- Interest Rates: A higher credit score results in lower interest rates on loans. Lenders view borrowers with higher scores as less risky, so they offer them loans with more favourable terms.

- Loan Approval: A good credit score increases your chances of quick loan approval. The banks are more likely to approve applications from individuals with a history of responsible credit use. With a credit score of less than 650, your loan is likely to be rejected.

- Loan Amount: A higher credit score can also influence the loan amount you’re eligible for. Lenders may be willing to offer larger loan amounts to borrowers with better credit histories. If you are taking a study abroad education loan then the amount is likely to be high.

- Repayment Terms: With a good credit score, you can negotiate with the bank for more flexible repayment terms, such as longer loan durations. This will help you in getting a lower amount of EMIs.

- Access to Various Loan Types: A strong credit score opens doors to a wider range of loan products like personal loans, mortgages, and credit cards. With a good credit score, you can even get add-on services from your bank such as forex cards, credit cards etc.

Also Read: Early Repayment Charges on Education Loan

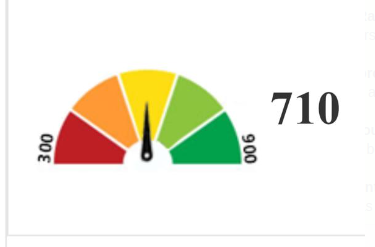

Credit Score Indicator

Credit score usually ranges from 300 to 900 and you get a score based on your repayment habit, account history, and credit inquiries. Please note that multiple credit enquiries also lead to a fall in your credit score. Always share the data with trusted financial institutions and banks and don’t make it a habit to check scores at a regular interval. Check the credit score indicator table below:

| Credit Score | Remarks | Impact on Loans |

| 300-579 | Poor | Very low chance of getting a loan |

| 580-669 | Fair | Low chances of getting a high amount of loan |

| 670-739 | Good | The loan may get approved with a short repayment period |

| 740-799 | Very Good | High chances of getting a loan with an attractive interest rate and a long repayment period |

| 800-850 | Exceptional | High rate of loan approval with maximum repayment period and affordable interest rates |

Note: The above-mentioned data is based on feedback and general practices and it doesn’t guarantee any approval or rejection. Always consult with a CA or financial advisor and contact your bank to understand the major terms and conditions.

FAQs

A credit score above 650-700 is usually considered a good credit score. However, it may vary from bank to bank depending on the terms and conditions. Some banks may not approve a loan if you have a credit score below 700.

You can get an education loan even if you don’t have a credit score yet. The bank may consider the credit history of the co-applicant in this case. However, you can build your credit history by taking a small amount of personal loan and repaying it properly.

You can get a Forex card with a credit score of 650 but with limited options. However, it depends upon the bank or financial institution about what score they are considering for approval.

This was all about ‘Credit Scores and Their Impact on Education Loan Refinancing.’ Credit score impacts your education loan refinancing directly and it is one of the most important parameters for the approval of your loan. Always pay your EMIs and credit card bills on time without any delay. This will help you improve your credit score fairly.

To know more about education loan refinancing, the best international bank accounts for students, forex and banking experience for global students or international money transfers, reach out to our experts at 1800572126 to help ease your study abroad experience.

| Related Blog |

| Education Loan Interest Rates |

| Personal Loan Vs Education Loan |

| Education Loan Disbursement Process |

Follow Us on Social Media