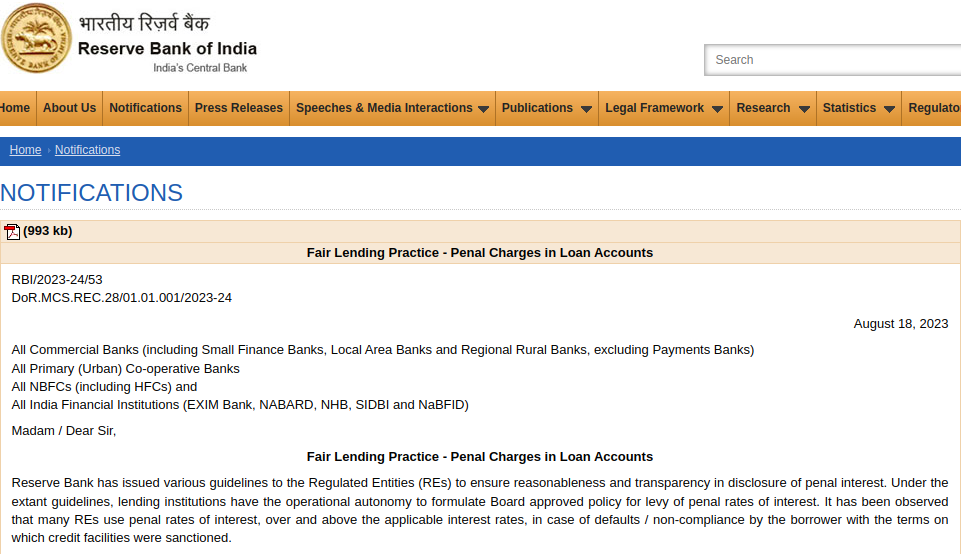

The new penal charges regime which was supposed to be implemented on January 1, 2024, has been extended to April 1, 2024, by the Reserve Bank of India. The extension will be applicable only to new loans. However, all the old loans will be under the new penal charges regime by June 30, 2024. The circular for the same was released by the central bank on Friday. The new penal charges guidelines will be applicable to all commercial banks, primary cooperative banks, NBFCs and All India Financial Institutions under EXIM Bank, NABARD, NHB, SIDBI and NaBFID).

Found error in your credit report? Read Here about the recent RBI regulations on credit report

What is Penal Charge in Loan Accounts?

In case of a delay in payment of EMI or any other payment against a loan, the borrower is liable to pay additional interest and other types of charges. This is called penal charge which is levied by the financial institutions or banks in line with the guidelines of the RBI. The central bank has issued a set of guidelines to all the regulated banks and NBFCs to ensure reasonableness and transparency in its disclosure. Check some of the major factors below:

- Under the existing guidelines, the banks or any lending institutions have the autonomy to implement policies approved by the board for the levy of penal rates of interest.

- The Reserve Bank of India has noticed that many regulated entities use penal rates of interest more than the applicable interest rates.

- This majorly happens in case of any education loan defaults or any other loan default or non-compliance by the borrower with the terms of the loan or any credit facilities that were sanctioned.

Are you aware of the guidelines set by RBI under restructuring scheme 2.0? Check here some of the common FAQs on Restructuring Scheme of RBI

Purpose of Penal Charges in Loan Accounts

Penal charges are levied so that the customers can develop a sense of credit discipline while repaying the loans or any kind of debt. Also, the customers will understand the importance of good credit score and how it will negatively impact if loans are not being paid on time. However, some organisation charges more interest and penalties than directed. As per the RBI, the penal charges are important to maintain the credit discipline but banks or financial institutions shall not make this a revenue generating tool. In the review process, the central bank has got things that indicate divergent practices amongst the regulated entities regarding the levy of penal interest and charges leading to customer grievances and disputes.

The new penal interest regime is applicable for all types of loans provided by any regulated entity or financial institution operating in India. Also, all the instructions under the new regulation will not be applicable for credit cards which are covered under product-specific directions. Stay informed and report such things on the official website of RBI, if required.

Follow the Fly Finance Newsdesk to get regular updates on study abroad loans, the latest guidelines, international money transfers etc.