Understanding part-period interest in education loans is crucial for effective financial planning. This interest accrues between the loan disbursement date and the commencement of the repayment schedule, often during the grace or moratorium period post-graduation. Being aware of this component helps borrowers anticipate additional costs and manage their finances more efficiently.

Part-period interest in education loans is typically included in the EMI, but you have the option to pay it upfront to reduce future financial stress. Let’s explore what part-period interest in an education loan entails, along with the reasons and methods for its application by banks.

Table of contents

What is Part Period Interest in an Education Loan?

Part-period interest in education loans refers to the interest charged by the bank or the lender for the period between loan disbursement and the date of commencement of the repayment schedule. In simpler terms, it is the interest accrued while the borrower is still in a grace period or moratorium period after graduation.

To better understand how part-period interest works and its implications, let’s explore key concepts like the grace period, scenarios where it applies, and how it is calculated.

- Understanding the Grace or Moratorium Period: This type of interest typically accrues during the grace period or moratorium period, while the borrower has yet to begin repayments after completing their education.

- Part-Period Interest in Standard Loan Scenarios: Even for loans without a moratorium period, part-period interest is applicable. It is calculated for the gap between disbursement and EMI commencement.

- Example of Part-Period Interest Calculation: If a loan is disbursed on the 15th of one month and the EMI begins on the 5th of the following month, the lender will charge interest for the 20-21 days in between.

- Importance of Understanding Part-Period Interest: Knowing about this interest component helps borrowers plan better for additional costs and manage financial responsibilities effectively.

Also Read: Check here all the details on Government Education Loan to Study in USA

Why Does Part Period Interest in Education Loan Matter?

Grasping the concept of part-period interest in education loans is essential for understanding the additional costs that come alongside your EMI payments. Here’s why recognizing its significance is crucial:

- Accurate Financial Planning: Neglecting part-period interest can result in underestimating the total borrowing cost. Factoring in this interest helps students create precise budgets and financial plans.

- Reducing Future Burden: If you have surplus funds, paying off part-period interest early can prevent it from accumulating. This proactive approach avoids higher EMIs and minimizes financial strain in the long run.

Being aware of part-period interest ensures better financial preparedness and prevents unexpected costs during repayment. Let’s now understand the Long-Term Financial Impact and how to Avoid Surprises.

Long-term Financial Impact

Part-period interest in education loan increases the overall cost of an education loan, making it crucial for borrowers to understand its financial impact. Awareness of this component helps borrowers evaluate the long-term repayment implications and plan their loan repayment strategy effectively.

By staying informed about the additional charges imposed by the bank and how part-period interest affects EMI amounts, you can develop a well-structured plan to manage your repayment and reduce financial stress.

Avoiding Surprises

Lack of awareness about part-period interest in education loans can result in financial surprises post-graduation. By staying informed, students can anticipate and prepare for upcoming expenses. It will increase your financial burden if all of a sudden you will see the schedule of charge and an increase in EMI amount.

Also Read: Are you aware of the consequences of not paying EMIs timely? Check here all about Education Loan Default.

How to Calculate Part Period Interest in Education Loan?

It is very easy to calculate part-period interest rates in education loans. If you already know the terms and conditions of your education loan like the details about the interest rate, disbursement date, moratorium, and the start date of the repayment period, you can easily calculate the amount of interest that you will pay. Check the steps below:

- Verify the Loan Disbursement Date: Start by checking the date when the loan was transferred to your educational institution, as this marks the beginning of the part-period during which interest begins to accumulate.

- Identify the Repayment Start Date: Review your loan agreement to determine the exact date when your repayment schedule is set to begin. This date is crucial for calculating part-period interest.

- Calculate the Time Frame: Measure the number of days between the loan disbursement date and the repayment start date. This time frame represents the period over which part-period interest is charged.

- Use the Formula to Calculate Part-Period Interest: Apply the appropriate formula to determine the part-period interest and ensure you understand how it impacts your overall loan cost.

The formula to calculate part-period interest on an education loan is as follows:

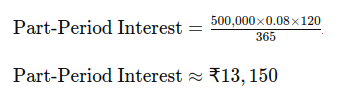

Part-Period Interest = (Loan Amount × Interest Rate × Number of Days) / 365

Where:

- Loan Amount = The principal amount borrowed.

- Interest Rate = The annual interest rate on the loan (in decimal form, e.g., 10% would be 0.10).

- Number of Days = The number of days for which the interest is calculated (can be the partial period between the disbursement date and EMI start date).

- 365 = The number of days in a year (used for daily interest calculation).

Example Calculation:

To better understand how part-period interest is calculated, let’s consider an example with the following details:

- Principal Amount: INR 5,00,000 (This is the amount you borrowed for your education.)

- Part-Period Interest Rate: The interest rate applicable during the part-period. This rate may differ from the standard interest rate and should be specified in your loan agreement (0.08%)

- Number of Days: 120 days (This is the time between when the loan is disbursed and when the repayment period starts.)

- 365: The total number of days in a year.

Using the formula:

This will give you the part-period interest amount to be paid, helping you understand the additional cost before regular loan payments begin.

Tips for Managing Part Period Interest in Education Loan Effectively

Effectively managing part-period interest in education loans is essential for maintaining a solid financial plan. Here are some actionable tips to help you handle part-period interest with ease:

- Familiarize Yourself with Loan Terms: Take the time to fully understand your education loan agreement, focusing on the specifics of part-period interest.

- Incorporate Interest into Your Budget: Plan ahead by including part-period interest in your budget and allocating funds to cover it, ensuring you’re financially ready when repayments begin.

- Explore Flexible Repayment Options: Some lenders provide options to start paying part-period interest while you’re still pursuing your education. This can help minimize the total interest burden.

- Utilize the Moratorium Period Wisely: If your loan offers a post-graduation moratorium, consider making voluntary payments toward part-period interest to prevent it from accumulating further.

- Monitor Your Interest Accrual: Regularly review your loan statements to stay informed about the interest charged during the part-period phase and stay on top of your financial responsibilities.

By adopting these strategies, you can reduce the financial impact of part-period interest and create a smoother repayment journey.

FAQs on Part Period Interest in Education Loan

Part-period interest refers to the interest accrued on an education loan during specific periods, such as the time between loan disbursement and the start of repayment or during a grace period after graduation. It is calculated based on the outstanding loan amount during this interim period.

Part-period interest in education loan is calculated using a simple interest formula based on the principal loan amount, the part-period interest rate, and the number of days in the part-period. Here’s the formula for calculating part-period interest:

Part-Period Interest = (Loan Amount × Part-Period Interest Rate × Number of Days) / 365

Part-period interest in education loan begins accruing from the date the loan funds are disbursed to the borrower or the educational institution. It continues to accrue until the start of the repayment period or the end of any grace period specified in the loan agreement.

Yes, part-period interest can apply to any education loan where the disbursement occurs before the repayment period begins, including those with grace periods or staggered disbursements.

Yes, borrowers have the option to pay off part-period interest early if they wish to do so. Some lenders may offer flexible repayment options that allow borrowers to make voluntary payments toward part-period interest, which can help reduce the overall interest burden over time.

Part-period interest adds to the total loan repayment amount, increasing the overall cost of borrowing. It is essential for borrowers to factor in part-period interest in education loan when planning their finances and budgeting for loan repayment to ensure they can manage their financial obligations effectively.

Part-period interest itself does not directly affect your credit score; however, failing to manage your loan payments, including part-period interest, can lead to missed payments and negatively impact your credit score.

While some lenders may have fixed policies regarding part-period interest, it is worth discussing your concerns with them. They might offer flexible options or clarify how you can minimize its impact.

If part-period interest is not paid, it may be added to your principal balance, leading to a higher total loan amount and increased future interest charges due to compounding.

Policies regarding part-period interest can vary widely among lenders. It’s advisable to compare terms from different financial institutions and read customer reviews to find one that offers favourable conditions regarding part-period interest.

You can manage part-period interest by budgeting for it in advance, paying it during the moratorium period, or opting for repayment options that allow interest payments while studying.

It is generally unavoidable; however, paying it early or choosing a loan scheme with interest waivers can help minimize its impact.

Yes, many lenders allow borrowers to pay part-period interest upfront, reducing the financial burden when repayment starts.

Part-period interest in education loan is an important aspect of education loans that every student studying abroad should understand. By understanding its implications and implementing effective financial management strategies, students can make their loan journey easy and minimize the long-term financial impact.

To know more about education loans, the best bank accounts for students, forex and banking experience for global students or international money transfers, reach out to our experts at 1800572126 to help ease your study abroad experience.

Follow Us on Social Media