Education loans are a go-to option for students who need help covering tuition and living costs. But what about the interest banks charge? It can be either fixed or floating, and it’s often influenced by factors like the repo rate or the marginal cost of funds.

Understanding the different types of interest rates and how they’re calculated is key to managing your loan. Curious to know more about what is education loan interest rate and how it works? Let’s break down the essential details of interest rates on education loans in this blog!

Table of contents

What is the Education Loan Interest Rate?

The education loan interest rate is the cost you pay for borrowing the money for your higher studies. It is the amount paid to the lender over and above the actual amount (also called the principal amount) you borrowed. The interest rate is usually expressed as a percentage of the principal loan amount.

For example, an education loan with an interest rate of 9.25% p.a means that the lender will charge you 9.25% of the loan amount every year. Let’s break it down a bit more clearly:

- 9.25% p.a. means 9.25% interest per year.

- If you borrow, say, an education loan of INR 10,00,000 (10 lakhs), after one year, the interest you owe would be INR 92,500 (9.25% of INR 10,00,000).

- This interest is added to the principal loan amount you borrowed and you’ll need to repay both the principal and the interest, which will be INR 10,92,500.

If the loan interest rate is simple interest, this amount remains the same each year. However, if it’s compound interest, the interest would keep adding to the total loan balance, and you’d pay interest on the increased amount.

Also Read: This blog includes the details about the Education Loan at 0% Interest Rate. To know more about it read the blog.

Types of Education Loan Interest Rate

There are primarily two types of interest rates on education loans: fixed and floating. The fixed interest rate remains constant throughout the loan term. On the other hand, the floating interest rate can change over time based on an external benchmark like the Repo Rate or MCLR.

Additionally, interest can be calculated using simple interest, where you pay interest only on the principal amount, or compound interest, where interest is calculated on both the principal and accumulated interest.

Each type has its advantages and drawbacks, and the choice depends on your financial situation and preference for stability or flexibility in repayment. Let’s get into the details on the types of education loan interest rates in this section of the blog-

Fixed Interest Rate

A fixed interest rate stays the same throughout the entire loan tenure. This means that the interest rate does not change, and your EMIs (Equated Monthly Installments) will remain the same every month.

Some lenders provide the option of choosing the type of fixed interest rate. You are entitled to the following benefits on fixed education loan interest rates-

- Since your monthly payments are fixed, it is easier to budget and plan your finances.

- You won’t have to worry about fluctuating interest rates during your loan term.

However, it is important to consider the other side as well and be aware of the disadvantages it can have on the education loans borrowed-

- Fixed rates are often a bit higher than floating rates, especially if market interest rates are low.

- If education loan interest rates drop due to changes in the market and economic conditions, you will still have to pay the interest rate that was fixed by the lender while lending you the education loan. You cannot benefit from a drop in interest rates in the market.

Floating Interest Rate

A floating interest rate on education loans keeps on changing. This is because it is tied to an external benchmark, such as the Repo Rate or MCLR, which changes periodically. When the benchmark rate changes, the floating interest rate will adjust accordingly, meaning your EMIs can fluctuate over time.

Choosing the floating interest rates gives you various benefits.

- If the external benchmark (like the repo rate) drops, your interest rate may reduce, lowering your EMIs.

- Floating rates are often lower at the start, compared to fixed rates.

However, this isn’t always the case. It is important to equally consider the disadvantages of floating rates-

- Your EMIs may increase if the benchmark rate rises, making it harder to plan your finances.

- In times of high inflation or interest rate hikes, you may face a significant rise in monthly payments.

Let’s continue to know more about the categories of floating interest rates. As discussed, they are based on the repo rate set by the RBI and the marginal costs of funds. Based on this, banks offer RLLR-based and MCLR-based floating interest rates on education loans. You can learn more about the calculation in our blog on student loan interest rates.

| Type of Floating Interest Rate | RLLR-based Floating Interest Rate | MCLR-based Floating Interest Rate |

| Full Form | Repo Linked Lending Rate (RLLR) | Marginal Cost of Funds-based Lending Rate (MCLR) |

| Linked To | Repo Rate (the rate at which RBI lends to banks) | The bank’s internal benchmark based on its cost of borrowing |

| Interest Rate Changes Based On | Changes in Repo Rate | Changes in MCLR, adjusted periodically (monthly/quarterly) |

| How It Works | The rate is set by adding a margin to the Repo Rate | The rate is set by adding a spread to the MCLR |

| Impact of Rate Changes | If Repo Rate decreases, EMIs decrease; if it increases, EMIs rise | If MCLR changes, EMIs change accordingly |

| Transparency | Transparent, as Repo Rate is set by RBI | Less transparent, as it’s based on internal bank costs |

| Stability | Less stable, as Repo Rate fluctuates with market conditions | More stable, as MCLR changes less frequently than Repo Rate |

Simple Interest Rate

The simple interest on education loans is the interest rate that is calculated only on the principal amount you borrow. It remains the same throughout the loan tenure.

It is calculated using the simple formula

Simple Interest = P × R × T, where

P = Principal loan amount

R = Interest rate per annum

T = Time in years

You can easily calculate the interest and understand how much you’ll owe. Also, since the interest is not compounded, the total amount of interest you pay will be less compared to compound interest.

For example, if the loan amount is INR 10,000 at an interest rate of 5% per year for 4 years, then the simple interest will be:

Simple interest- 10,000 × 0.05 × 4 = 2,000

Total amount to be repaid = INR 10,000 (Principal) + INR 2,000 (Interest) = INR 12,000

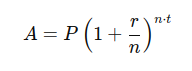

Compound Interest Rate

Compound interest is calculated on the initial principal as well as the accumulated interest from previous periods. This means the interest compounds (gets added to the principal) periodically (annually, monthly, etc.), increasing the loan balance over time.

It is calculated using the given formula-

where:

- A is the amount to be repaid (principal + interest),

- P is the principal loan amount,

- r is the interest rate per period,

- t is the time in years,

- n is the number of times the interest is compounded per year.

It is more complex than simple interest and results in higher total repayment amounts, especially over longer periods.

Impact of Education Loan Interest Rate on Repayment

Your education loan repayment amount is directly impacted by the interest rate applied. A lower interest rate means lower monthly payments, which can help ease your financial burden. Similarly, a higher interest rate results in higher repayments, increasing the total cost of your education loan.

Here’s how different interest rates can impact your total repayment:

- A loan of INR 5,00,000 at 10% p.a for 10 years could cost you INR 8,00,000 in total repayment.

- A loan of INR 5,00,000 at 6% for 10 years could cost you INR 6,80,000 in total repayment.

Also Read: This blog includes the details about the Education Loan for PG Abroad. For more details about it check out our blog.

Factors Affecting Education Loan Interest Rates

When you’re applying for an education loan, the interest rate can feel like a mystery. But it’s not just random — it’s shaped by several key factors. Some of these factors are the lender’s policies, type of loan, your CIBIL score, loan tenure, and market conditions. Let’s understand how they determine the interest rate applicable to your education loan.

- Lender’s Policy- Banks and financial institutions decide the interest rate based on their goals. Some may offer lower rates to attract more customers, while others may have higher rates depending on their business strategy. Some of the banks offering lower interest rates on education loans are Bank of Baroda, PNB, SBI, etc.

- Type of Loan- Government loans typically come with lower interest rates compared to private loans. This is because the government backs these loans, making them less risky for lenders.

- Your Credit Score- Think of your credit score as your financial reputation. A higher score means you’re a reliable borrower, so lenders reward you with a lower interest rate. A lower score might result in a higher rate because you’re seen as a riskier investment.

- Loan Term- Longer loan terms generally mean higher interest rates. Why? Because the longer you take to repay, the more likely economic conditions might change, and lenders want to ensure they’re covered for the long haul.

- Market Conditions- Interest rates also reflect the broader economy. When inflation is high, interest rates tend to go up. If the central bank raises rates to control inflation, your loan rate could rise too.

How to Get the Best Education Loan Interest Rate?

Securing the best education loan interest rate can make a big difference in how much you pay back over time. Here’s how to snag the lowest rate possible:

- Compare Lenders- Different banks and financial institutions offer varying interest rates. You should not settle for the first offer, instead to find the best interest rates you should explore and compare education loan interest rates of different banks and NBFCs and find the most competitive rate.

- Maintain a Good Credit Score- A strong credit score shows lenders you’re financially responsible. The higher your score, the lower your interest rate is likely to be. So, work on improving your credit score before applying for a loan.

- Consider Government Loans- Government-backed education loans typically offer lower interest rates compared to private loans. If you’re eligible for these, they’re often your best bet.

- Check for Special Offers- Some banks offer discounts on interest rates for students with good academic records or if you have a co-signer. Keep an eye out for these opportunities.

- Understand Loan Terms- The length of your loan can affect your interest rate. Shorter-term loans often come with lower rates, while longer ones might have higher rates.

This was all about what is education loan interest rates and related details. By understanding how interest rates work, and carefully selecting the right type and terms of your loan, you can ensure that your education financing is manageable. Remember to compare rates, consider all factors, and choose a loan that best aligns with your repayment capacity and long-term goals.

To learn more about education loans, the best bank accounts for students, forex, banking experience for global students, or international money transfers, reach out to our experts at 1800572126 to help ease your experience with studying abroad.

FAQs

An education loan interest rate is the percentage charged by a lender on the loan amount, which you repay along with the principal over time.

There are two types: fixed (remains the same throughout the loan term) and floating (varies with market conditions).

Fixed rates offer stability with predictable payments, while floating rates can change based on market conditions, potentially offering lower rates initially but with some risk.

Key factors include your credit score, loan amount, repayment tenure, lender policies, and whether the loan is government-backed or private.

Some banks with competitive rates include State Bank of India (SBI), HDFC Bank, ICICI Bank, and Axis Bank, with rates starting from 10.25% p.a.

A higher credit score (750+) can help secure a lower interest rate, as it indicates you’re a lower-risk borrower. This helps you get a higher loan amount at attractive interest rates.

Education loan interest rates typically range from 9% to 15%, depending on whether the loan is for domestic or foreign education and the lender.

Yes, if you have a floating interest rate loan, the rate can change depending on market fluctuations or the lender’s base rate.

Yes, government-backed education loans generally offer lower rates compared to private loans, making them a more affordable option for students.

Some banks may allow negotiation, especially if you have a strong credit history, a co-signer, or are applying for a large loan amount. Fly Finance helps you get the best interest rates and negotiates on your behalf to get the best deals possible for your education loan abroad.

Follow Us on Social Media