RRN Full Form: In the digital age, acronyms like RRN pop up on bank statements, payment apps, or receipts. RRN is a 12-digit code that tracks financial transactions like UPI payments, card swipes, or online purchases. But what does RRN full form mean, and why should you care?

Understanding the meaning of RRN can help you navigate banking systems, resolve payment disputes, and ensure secure transactions. In this guide, we will cover the full form of RRN, its meaning and its importance.

Table of contents

What is the Full Form of RRN?

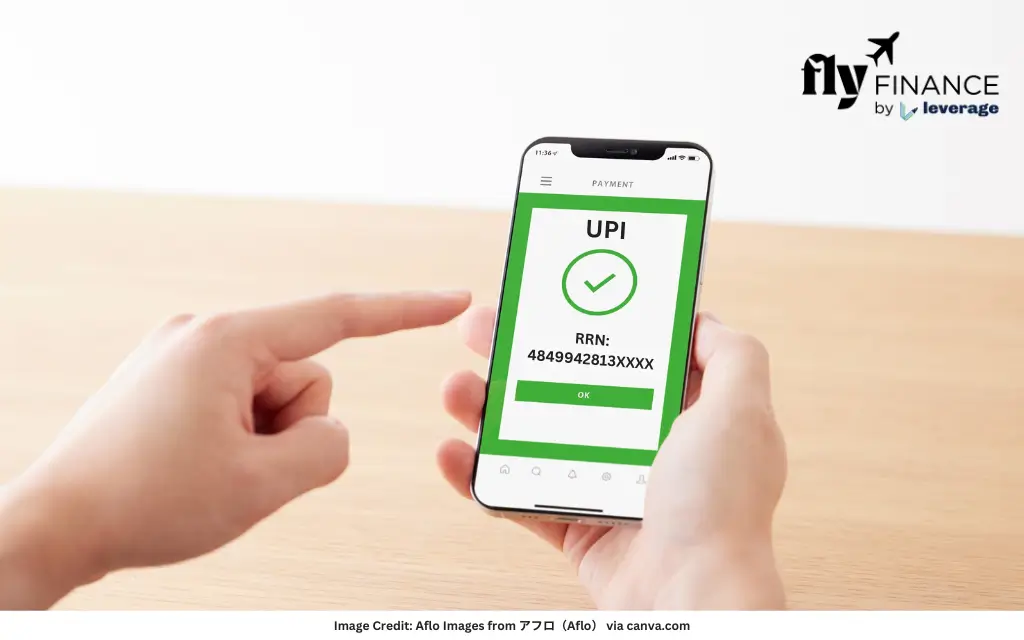

The RRN full form stands for Retrieval Reference Number. It’s a special 12-digit number that tags every payment you make. Banks and UPI (Unified Payments Interface) apps use it to keep things organised. It follows a global rule called ISO 8583, which helps card and online payments work smoothly.

In India’s UPI ecosystem, for example, it is often called the UPI Reference Number. When you pay through UPI apps, this number ensures that your money reaches the intended recipient.

The Retrieval Reference Number simplifies payment verification and helps financial systems operate smoothly, making it a crucial component of modern banking.

Also Read: PAN Full Form: Documents, Eligibility, How to Apply, Importance

Why Does RRN Matter?

The Retrieval Reference Number saves the day in many ways. Imagine you send cash via UPI app, but it doesn’t reach your friend. Share the RRN with your bank—they’ll track it down. It proves you paid and fixes mix-ups like failed transfers or extra charges.

RRN number also keeps your payments safe. With tons of transactions happening daily, it stops confusion. Whether you’re shopping or running a business, the RRN helps you sort out money issues quickly.

How Does RRN Work in UPI Payments?

In India, the Retrieval Reference Number powers UPI transactions. With over 121 billion payments processed in 2023 (per NPCI), UPI relies on this payment identifier. When you send cash by scanning a QR code or entering a UPI ID, the system generates a 12-digit RRN, like 123456789012.

RRN number ties your bank, the recipient’s account, and the transaction details together, processed via NPCI servers. It’s a seamless way to ensure payment success. Next time you use any UPI app, look for this UPI reference in your history—it’s the RRN at work.

How to Locate Your RRN?

Finding your Retrieval Reference Number is straightforward. For UPI payments, open your UPI app, go to transaction history, and tap a payment. You will see the RRN, often labeled UPI Ref No.. On bank statements, it’s next to the amount and date. SMS alerts might say: “Paid Rs. 500. Ref No: 123456789012.”

For card purchases, peek at your merchant receipt or email invoice—the RRN’s usually listed. Knowing where to find this financial code helps with payment disputes or verification. Try it with your latest transaction!

Do you know: RRN and UTR number are unique identifiers that help banks and customers track and verify transactions in case of disputes or failures. UTR is used for tracking NEFT, RTGS, and IMPS transactions, while the RRN is used for card-based and UPI transactions.

An Example of RRN

Let’s say you’re Priya, a shop owner. A customer pays INR 1,500 via any UYPI app, but your account stays empty. Ask for the RRN which will appear like this “RRN: 980604311098 or UPI Ref No: 980604311098”.

After that, you call your bank, share the payment number, and they find the glitch. By EOD, your cash arrives.

This proves the Retrieval Reference Number connects you to payment systems. It’s your fix for money troubles in real time.

Also Read: BSBDA Full Form: Features and Why it is Important?

Other Meanings of RRN

The RRN full form is usually the Retrieval Reference Number in finance, but it changes depending on the field. In telecom, RRN can mean Radio Relay Network, used for signal relays.

In health, the RRN might be the Recovery Research Network studies well-being. In techIn or AI, Random Recurrent Neural Network is another rare use.

RRN vs. Transaction ID: What’s Different?

People mix up the Retrieval Reference Number with a Transaction ID, but they’re not the same. Ever wondered how the Retrieval Reference Number differs from a Transaction ID? The RRN is a universal payment tag from systems like NPCI, while a Transaction ID (e.g., “TXN12345”) is often bank-specific and internal.

For example, your UPI app might show an RRN like 678901234567 for merchant use, but your bank logs a separate reference number. Both help with financial tracking, but the RRN’s reach is wider in payment networks.

Tips for Using RRN Smartly

Here’s how to leverage the Retrieval Reference Number: Save RRN after each payment confirmation by taking its screenshots. Share it for dispute resolution to speed things up. Verify it on receipts for transaction accuracy.

Whether it’s a UPI glitch or a card issue, this payment code is your friend. Start using it wisely today!

The RRN full form is Retrieval Reference Number, it is your secret weapon in digital payments. RRN is a 12-digit helper that secures UPI transfers, fixes bank mix-ups, and keeps cash flowing right. Now you can spot it in your app and use it like a pro.

FAQs on RRN Full Form

The RRN full form stands for Retrieval Reference Number, a unique 12-digit code assigned to financial transactions. It helps banks, UPI apps, and card networks track payments, resolve disputes, and ensure smooth processing of digital transactions.

In UPI payments, the Retrieval Reference Number (RRN) acts as a transaction identifier that helps NPCI and banks verify and process payments. This number is crucial for tracking failed or delayed transactions, ensuring accuracy in digital fund transfers.

To locate your RRN UPI reference number, open your UPI app and navigate to the transaction history section. The RRN is usually labeled as “UPI Ref No.” or “Transaction Reference” and is displayed next to the payment details.

The Retrieval Reference Number (RRN) plays a key role in secure online payments by providing a unique tracking code for each transaction. It helps customers and banks verify payments, resolve issues like failed transactions, and prevent financial fraud.

No, the RRN full form refers to Retrieval Reference Number, a globally recognized tracking code, whereas a Transaction ID is a bank-specific reference number. While both help in tracking payments, RRN is widely used across payment networks like NPCI.

If a payment fails or remains pending, the Retrieval Reference Number (RRN) allows banks to trace the transaction and identify the issue. Customers can share the RRN with their bank’s customer support to expedite refunds or resolve disputes efficiently.

Yes, the RRN applies to card transactions as well, appearing on bank statements and merchant receipts. Whether it’s a credit or debit card payment, this number helps track purchases, process refunds, and verify payment records.

Yes, every financial transaction, whether through UPI, card swipes, or online banking, is assigned a unique 12-digit Retrieval Reference Number (RRN). This ensures proper tracking, fraud prevention, and easy resolution of any payment-related concerns.

The Retrieval Reference Number (RRN) is mainly used for UPI and card transactions, while the Unique Transaction Reference (UTR) Number is assigned to NEFT, RTGS, and IMPS bank transfers. Both help in tracking payments but are used in different financial systems.

Businesses can use the Retrieval Reference Number (RRN) to verify successful payments, manage refunds, and handle disputes more efficiently. By tracking transactions with RRN, businesses ensure smooth financial operations and maintain transparency with customers.

To learn more about bank accounts for students, the best education loans, forex, banking experience for global students, or international money transfers, reach out to our experts at 1800572126 to help ease your experience with studying abroad.

Follow Us on Social Media